Sukanya Samriddhi Yojana

The Sukanya Samriddhi Yojana (SSY) is a government-backed savings system that aims to empower girls in India. It was introduced in 2015 as the main project within the "Beti Bachao, Beti Padhao" (BBBP) campaign.

This scheme aims to provide a secure and rewarding way for parents to save for their daughters' education and future, helping them achieve financial independence.

Open an SSY Account

- Step 1: First step is to visit a participating bank or post office, choose a branch that is convenient for you.

- Step 2: Provide accurate details about the girl child and the guardian.

- Step 3: Attach the required documents:

- Birth certificate of the girl child

- Identity and address proof of the guardian (e.g., Aadhaar card, PAN card, passport, driving license)

- Passport-sized photographs of the girl child and guardian

- Medical certificate (in case of multiple girl children in a single birth order)

- Step 4: Make your initial deposit. Remember, the initial deposit should be between ₹250 and ₹1.5 lakh.

- Step 5: Once the application and deposit are processed, you will receive a passbook for the SSY account.

Online Payment

For added convenience, you can make online payments towards your SSY account using the IPPB app. Simply transfer funds from your bank account to your IPPB account and set up standing instructions for automatic payments.

Open Account Through Banks

You can open an SSY account at authorized commercial banks that offer this scheme. The process is similar to opening an account at a post office and requires the same documents. You can visit the respective bank's website to download the SSY account opening form or obtain it from the branch.

Banks That Offer SSY Accounts:

The SSY is available at a wide range of banks and post offices across India. Some of the major banks offering SSY accounts include:

- State Bank of India (SBI)

- ICICI Bank

- HDFC Bank

- Kotak Mahindra Bank

- Axis Bank

- Bank of Baroda

- Indian Bank

- UCO Bank

- Punjab National Bank

- Canara Bank

- Union Bank of India

- Indian Overseas Bank

- Central Bank of India

- Bank of Maharashtra

- Syndicate Bank

- Oriental Bank of Commerce

- IDBI Bank

- Vijaya Bank

- Corporation Bank

- Dena Bank

- Allahabad Bank

- Andhra Bank

- Punjab and Sind Bank

- Bank of India

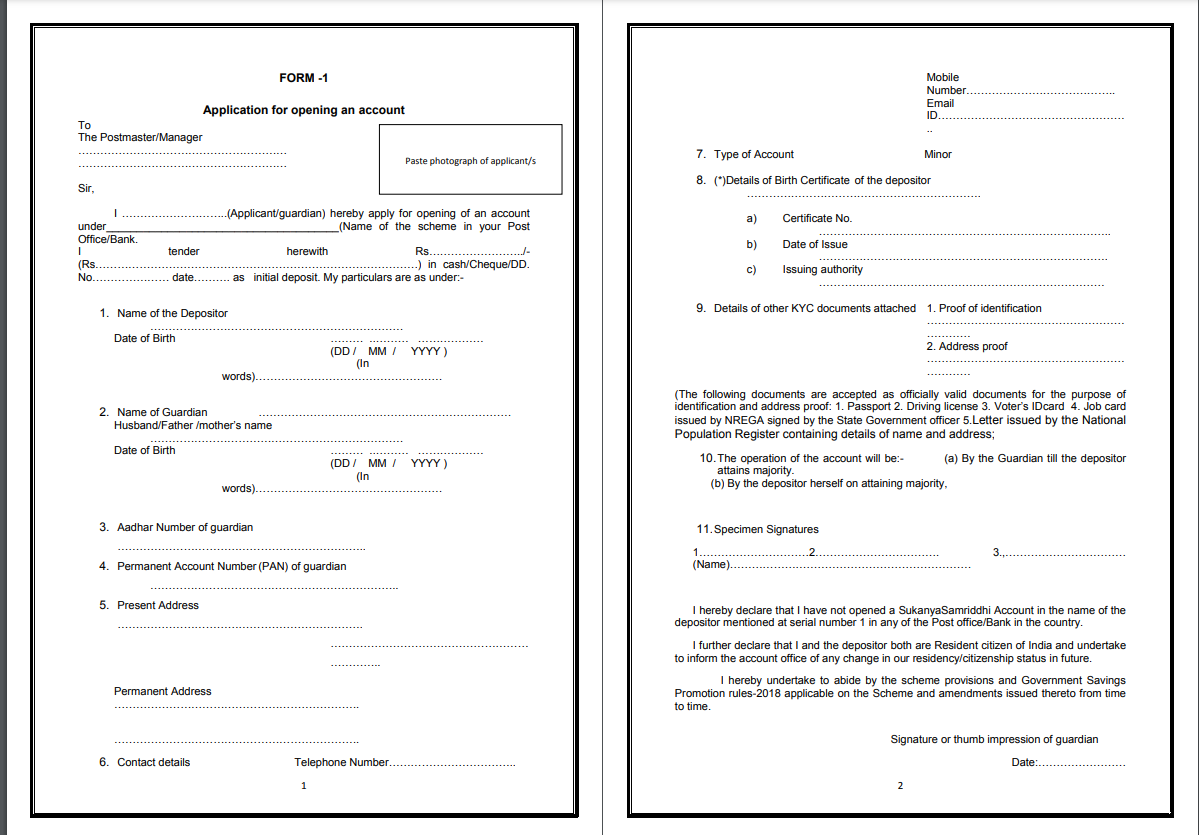

Application Form

The account opening form (Form-1) requires you to provide the following details:

- Post Office/bank branch details

- Applicant's photograph

- Deposit amount and payment mode

- Girl child's name and date of birth

- Guardian's name, date of birth, Aadhaar number, and PAN

- Address and contact details

- Details of birth certificate and KYC documents

- Signature and nomination details

Transfer of account

Process of Transferring a Sukanya Samriddhi Account from Post Office to Bank:

- Step 1: Go to the post office or bank where the account is currently held.

- Step 2: Inform the officials about your intention to transfer the account.

- Step 3: Fill out the account transfer form and provide the passbook and KYC documents.

- Step 4: Now go to the bank or post office where you want to transfer the account.

- Step 5: Submit the documents provided by the previous institution and complete any additional paperwork required.

Calculator

Interest is calculated yearly on the lowest balance between the 5th and the last day of each month. You can use online calculators or the formula A = P(1+r/n)^nt to estimate the maturity amount, where:

- P = Initial Deposit

- r = Rate of interest

- n = Number of years the interest compounds

- t = Number of years

- A = Amount at maturity

Total Investment:

Total Interest:

Maturity Year:

Maturity Amount:

What is Sukanya Samriddhi Yojana?

The Sukanya Samriddhi Yojana (Girl Child Prosperity Account) was launched by Prime Minister Narendra Modi on January 22, 2015, in Panipat, Haryana. This scheme allows accounts to be opened at any India Post office or authorized commercial bank branches.

Parents or guardians can open an account anytime between the birth of a girl child and the time she turns 10 years old. Each child is allowed only one account, with a maximum of two accounts per family, except in the case of twins or triplets where up to three accounts can be opened.

Objectives

In reaction to the serious issues of falling child sex ratios and the socioeconomic inequalities that Indian girls had to deal with, the SSY was established. It is a symbol of the government's commitment to safeguarding girls' well-being and equitable opportunity.

- Financial Security: Create a dedicated financial corpus for the girl child's future education and marriage expenses.

- Incentivize Savings: Encourage parents and guardians to invest in their daughter's future through attractive interest rates and tax benefits.

- Promote Gender Equality: Contribute to the larger goal of gender equality by empowering girls financially and reducing their dependency.

Eligibility Criteria

For the Child (Account Holder):

- The scheme is exclusively available to girl children.

- The girl child must be under the age of 10 years, with a grace period of one year.

For the Parents/Guardians:

- Only biological parents or legal guardians can open an account on behalf of the girl child.

- A parent or guardian can open up to two accounts, one for each girl child.

- In the case of twins or triplets, up to three accounts can be opened.

- The account holder must be an Indian citizen residing in India at the time of opening the account and must continue to be a resident until the account matures or is closed.

Features

The SSY offers an array of features that make it a compelling investment option for parents and guardians:

- Account Opening: Accounts can be easily opened at any post office or authorized commercial bank branch with minimal documentation.

- Flexible Deposits: The scheme allows for flexible deposits, with a minimum annual deposit of ₹250 and a maximum of ₹1.5 lakh. Deposits can be made yearly in multiples of ₹50.

- High-Interest Rate: The SSY boasts one of the highest interest rates among small savings schemes, currently at 8.2% per annum (Q1 FY 2024-25). The interest rate is subject to quarterly revisions by the government.

- Tax Benefits:

- Deduction under Section 80C: Deposits up to ₹1.5 lakh per year are eligible for deductions under Section 80C of the Income Tax Act.

- Tax Exemption: The interest earned and maturity amount are entirely exempt from tax.

- Maturity Period: The account matures after 21 years from the date of opening or upon the girl child's marriage after attaining 18 years of age, whichever is earlier.

- Partial Withdrawal: For the girl child's education expenses, 50% of the balance at the end of the previous financial year can be withdrawn after she turns 18 or passes 10th standard.

- Premature Closure: Allowed under specific circumstances like the girl child's demise, medical emergency, or if the account causes undue hardship.

- Account Transfer: The SSY account is easily transferable between post offices and banks anywhere in India.

- Online Payment: The India Post Payments Bank (IPPB) app facilitates seamless online payments for added convenience.

Interest Rate 2024

The SSY interest rate is reviewed and revised quarterly by the government. As of Q1 FY 2024-25 (April to June 2024), the interest rate is 8.2% per annum.

This is one of the highest interest rates offered among comparable savings schemes, making it an attractive investment option.

Interest Rates Revisions

| Financial Year | Date Range | Interest Rate | Minimum Investment | Maximum Investment |

|---|---|---|---|---|

| 2014–15 | 1 April 2014 to 31 March 2015 | 9.1% | ₹1,000 | ₹1,50,000 |

| 2015–16 | 1 April 2015 to 31 March 2016 | 9.2% | ₹1,000 | ₹1,50,000 |

| 2016–17 | 1 April 2016 to 30 September 2016 | 8.6% | ₹1,000 | ₹1,50,000 |

| 2016–17 | 1 October 2016 to 31 March 2017 | 8.5% | ₹1,000 | ₹1,50,000 |

| 2017–18 | 1 April 2017 to 30 June 2017 | 8.4% | ₹1,000 | ₹1,50,000 |

| 2017–18 | 1 July 2017 to 31 December 2017 | 8.3% | ₹1,000 | ₹1,50,000 |

| 2017–18 | 1 January 2018 to 31 March 2018 | 8.1% | ₹1,000 | ₹1,50,000 |

| 2018–19 | 1 April 2018 to 30 September 2018 | 8.1% | ₹250 | ₹1,50,000 |

| 2018–19 | 1 October 2018 to 31 March 2019 | 8.5% | ₹250 | ₹1,50,000 |

| 2019–20 | 1 April 2019 to 30 June 2019 | 8.5% | ₹250 | ₹1,50,000 |

| 2019–20 | 1 July 2019 to 31 March 2020 | 8.4% | ₹250 | ₹1,50,000 |

| 2020–21 | 1 April 2020 to 31 March 2021 | 7.6% | ₹250 | ₹1,50,000 |

| 2021–22 | 1 April 2021 to 31 March 2022 | 7.6% | ₹250 | ₹1,50,000 |

| 2022–23 | 1 April 2022 to 31 March 2023 | 7.6% | ₹250 | ₹1,50,000 |

| 2023–24 | 1 April 2023 to 31 December 2023 | 8.0% | ₹250 | ₹1,50,000 |

| 2023–24 | 1 January 2024 to 31 March 2024 | 8.2% | ₹250 | ₹1,50,000 |

| 2024–25 | 1 April 2024 to 30 June 2024 | 8.2% | ₹250 | ₹1,50,000 |

Conditions for Non-Payment

There are certain conditions under which interest may not be paid on the SSY account:

- Account Default: If the minimum annual deposit of ₹250 is not made, the account is considered in default, and no interest will be earned until it's regularized.

- Maturity: After the account reaches maturity (21 years or marriage after 18 years), no further interest is accrued.

- Non-Resident/Non-Citizen: If the girl child becomes a non-resident or non-citizen of India, interest will not accrue on the account thereafter.

Withdrawal Rules

Withdrawals are permitted under specific circumstances:

- Marriage: After the girl child turns 18, you can withdraw up to 50% of the balance at the end of the previous financial year for marriage expenses.

- Higher Education: Similar to marriage, 50% of the previous year's balance can be withdrawn for higher education expenses after the girl child turns 18 or passes 10th standard.

- Proof of Requirement: Documentary proof, such as a marriage certificate or admission proof to an educational institution, is required for withdrawals.

Closure Rules

The SSY account can be closed under the following circumstances:

- Maturity: Upon maturity, the account holder (girl child) can close the account by submitting the required documents.

- Premature Closure:

- Death of the girl child

- Medical treatment of life-threatening disease of the girl child or guardian

- Change in the girl child's residency status (becoming a non-resident or non-citizen)

- Extreme compassionate grounds (as determined by the government).